“Types of home insurance

Artikel Terkait Types of home insurance

Pengantar

Dalam kesempatan yang istimewa ini, kami dengan gembira akan mengulas topik menarik yang terkait dengan Types of home insurance. Mari kita merajut informasi yang menarik dan memberikan pandangan baru kepada pembaca.

Table of Content

Video tentang Types of home insurance

However, this significant investment requires equally significant protection. Home insurance, often referred to as homeowner’s insurance or dwelling insurance, is a crucial safety net that safeguards your property and financial well-being against unforeseen events. Understanding the various types of home insurance available is paramount to making an informed decision and securing the right coverage for your specific needs. This comprehensive guide will delve into the different types, their coverage specifics, and factors to consider when choosing the best policy for your home.

I. Understanding the Foundation: Basic Home Insurance Coverage

Before exploring the specialized types, it’s essential to grasp the core components of a standard homeowner’s insurance policy. Most policies encompass several key areas:

-

Dwelling Coverage: This is the cornerstone of your policy, covering the physical structure of your home, including the attached structures like garages and porches, against damage from covered perils such as fire, windstorms, hail, vandalism, and lightning. The coverage amount is typically based on the replacement cost of your home, not its market value.

-

Other Structures Coverage: This extends protection to detached structures on your property, such as a shed, fence, or detached garage. Coverage is usually a percentage of your dwelling coverage.

Personal Property Coverage: This protects your belongings inside your home, including furniture, electronics, clothing, and other personal items. Coverage is often based on a percentage of your dwelling coverage, and there may be limits on specific high-value items.

-

Liability Coverage: This crucial component protects you financially if someone is injured on your property or if you accidentally damage someone else’s property. It covers legal fees and any resulting settlements or judgments.

-

Medical Payments Coverage: This covers the medical expenses of anyone injured on your property, regardless of fault. This is a separate coverage from liability and can be crucial in minimizing legal complications.

-

Loss of Use Coverage: This covers additional living expenses if your home becomes uninhabitable due to a covered loss, such as a fire or major storm. This can include temporary housing, meals, and other essential expenses.

II. Delving Deeper: Specialized Types of Home Insurance

Beyond the standard policy, various specialized types of home insurance cater to specific needs and circumstances:

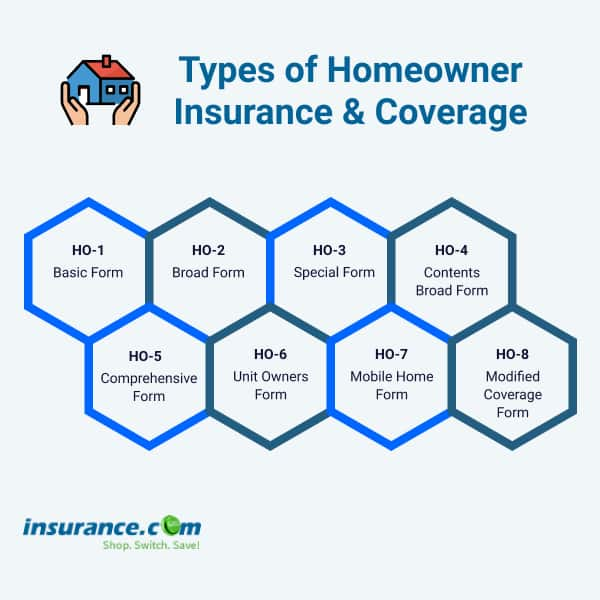

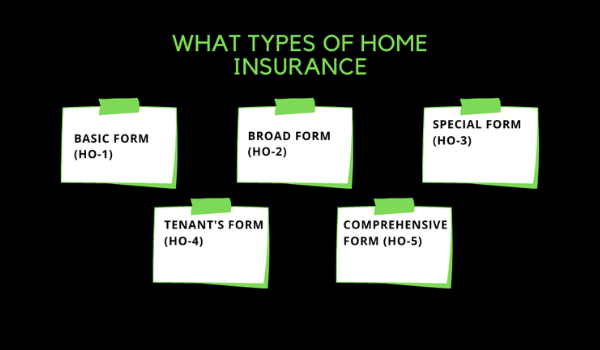

A. HO-1 (Basic Form): This is the most basic type of homeowner’s insurance, offering limited coverage for named perils. It typically covers only damage caused by specific events listed in the policy, such as fire, lightning, and windstorms. It offers minimal coverage and is rarely offered as a new policy.

B. HO-2 (Broad Form): This policy expands coverage beyond the named perils of the HO-1, including additional perils like falling objects, weight of ice, snow, and accidental discharge of water. It still offers less comprehensive coverage than more extensive policies.

C. HO-3 (Special Form): This is the most common type of homeowner’s insurance, offering broad coverage for all perils except those specifically excluded in the policy. This provides a higher level of protection against unforeseen events.

D. HO-4 (Renters Insurance): This policy protects renters’ personal belongings and provides liability coverage. It does not cover the building itself, as that is the responsibility of the landlord’s insurance.

E. HO-5 (Comprehensive Form): This is the most comprehensive type of homeowner’s insurance, offering open-peril coverage for both the dwelling and personal property. It protects against nearly all perils, except those specifically excluded in the policy. This offers the highest level of protection but typically comes with a higher premium.

F. HO-6 (Condominium Insurance): This policy covers the interior of a condominium unit and personal property, but it does not cover the building’s structure or common areas. The homeowner’s association typically handles insurance for the building itself.

G. HO-8 (Modified Coverage Form): This is designed for older homes that are difficult to insure under standard policies due to their age and condition. It offers a more limited coverage than other forms, typically using a market value approach rather than replacement cost.

III. Beyond the Basics: Additional Coverages and Endorsements

Standard home insurance policies can often be enhanced with additional coverages or endorsements to address specific needs:

-

Flood Insurance: This is a separate policy, often required by lenders in flood-prone areas. It covers damage caused by flooding, which is typically excluded from standard homeowner’s policies.

-

Earthquake Insurance: Similar to flood insurance, earthquake insurance is usually a separate policy and covers damage caused by earthquakes. It’s crucial in earthquake-prone regions.

-

Hurricane Insurance: In hurricane-prone areas, specific hurricane coverage may be necessary, often as an endorsement to a standard policy.

-

Personal Umbrella Liability Insurance: This provides additional liability coverage beyond the limits of your homeowner’s policy, offering greater protection against significant liability claims.

-

Scheduled Personal Property Coverage: This provides additional coverage for high-value items such as jewelry, art, or collectibles, often with agreed-upon values.

-

Identity Theft Coverage: This covers expenses associated with recovering from identity theft, a growing concern in today’s digital age.

IV. Factors to Consider When Choosing Home Insurance

Selecting the right home insurance policy requires careful consideration of several factors:

-

Coverage Amount: Determine the appropriate coverage amount for your dwelling, other structures, and personal property, ensuring adequate protection against potential losses.

-

Deductible: The deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible typically results in lower premiums, but you’ll bear more risk.

-

Premium Costs: Compare premiums from multiple insurers to find the best value for your needs. Factors influencing premiums include location, coverage level, and the age and condition of your home.

-

Insurer Reputation: Research the financial stability and customer service ratings of different insurers before making a decision.

-

Policy Exclusions: Carefully review the policy exclusions to understand what is not covered. This will help you identify potential gaps in your coverage.

-

Review and Update: Regularly review your policy to ensure it continues to meet your needs as your circumstances change, such as home improvements or the acquisition of valuable possessions.

V. Conclusion: Protecting Your Most Valuable Asset

Home insurance is more than just a financial product; it’s a critical investment in protecting your most valuable asset – your home. By understanding the various types of home insurance, their coverage specifics, and the factors to consider when choosing a policy, you can make an informed decision that provides the right level of protection for your unique circumstances. Don’t hesitate to seek professional advice from an insurance agent to navigate the complexities of home insurance and secure the peace of mind that comes with knowing your home and belongings are adequately protected. Remember, the cost of inadequate coverage can far outweigh the cost of comprehensive protection.

Penutup

Dengan demikian, kami berharap artikel ini telah memberikan wawasan yang berharga tentang Types of home insurance. Kami berharap Anda menemukan artikel ini informatif dan bermanfaat. Sampai jumpa di artikel kami selanjutnya!