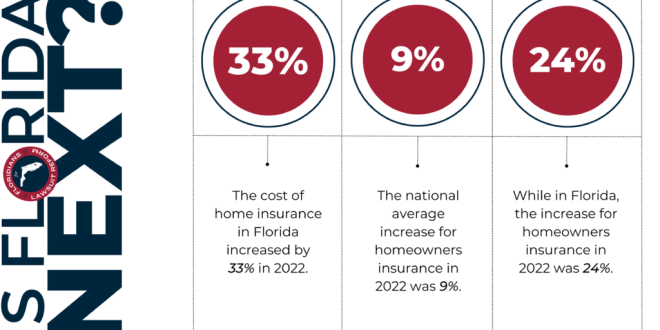

Homeowner’s insurance in Florida is a crucial investment, particularly given the state’s vulnerability to hurricanes. Understanding the factors that influence insurance costs and the challenges of securing coverage during hurricane season is essential for Florida homeowners to protect their properties and finances. This article will explore these aspects, offering insights into navigating the Florida insurance market and mitigating potential risks. Honestly, figuring out homeowner’s insurance here can feel like trying to solve a Rubik’s Cube blindfolded, especially with hurricane season looming.

Why is Homeowner’s Insurance So Expensive in Florida?

High Risk of Natural Disasters

Let’s face it, Florida’s got it all: sunshine, beaches, and unfortunately, a whole lotta natural disasters. Hurricanes, tropical storms, flooding, even sinkholes – you name it, we’ve probably got it. And all that risk? Yeah, it drives up your homeowner’s insurance faster than you can say “Category 5.” I mean, think about it. Insurance companies aren’t exactly thrilled about the prospect of paying out massive claims year after year. It’s just business, I guess, but it still stings when you see that premium.

Litigation and Fraud

Now, here’s a fun fact (not really): Florida’s also got a reputation for, shall we say, “creative” interpretations of insurance claims. Frivolous lawsuits and outright fraud? They’re a thing. And guess who ultimately pays the price? Yep, you do. All those bogus claims add up, and insurance companies pass those costs right back to policyholders like us. Makes you wonder if everyone’s playing fair, doesn’t it?

Reinsurance Costs

Okay, this one’s a bit wonky, but stick with me. Insurance companies, they need insurance too, right? It’s called reinsurance, and it’s basically insurance for insurance companies. In Florida, because of our, ahem, “active” weather, reinsurance is expensive. Like, really expensive. And guess what? That cost? Yep, it gets passed down to you in the form of higher premiums. It’s like a never-ending cycle!

Factors Affecting Your Homeowner’s Insurance Premium

Location

No surprise here. Where you live in Florida matters. Like, a lot. Closer to the coast? Boom, higher premiums. In a flood zone? Double boom. Hurricane-prone area? You guessed it, premiums through the roof. It’s all about risk assessment. The higher the risk of your house getting smacked by a hurricane or swallowed by a sinkhole, the more you’re gonna pay. Makes sense, but still…ouch!

Construction and Age of Home

So, picture this: you’ve got a shiny, new, hurricane-resistant house built to the latest codes. Or, you’ve got a charming, vintage bungalow built back in the day. Which one do you think is gonna be cheaper to insure? Yep, the newer one. Building materials, roof type, the age of your home – they all play a role. Older homes, especially those not built to withstand hurricane-force winds, are seen as higher risks.

Coverage Limits and Deductibles

This one’s pretty straightforward. The more coverage you want, the more you’re gonna pay. Want a policy that covers every single thing, no matter what? Get ready to shell out some serious cash. On the flip side, you can lower your premium by opting for a higher deductible. But remember, that means you’ll be paying more out-of-pocket if something does happen. It’s a balancing act.

Credit Score

Believe it or not, your credit score can actually influence your homeowner’s insurance rates in Florida. I know, right? Seems totally unrelated, but insurance companies argue that people with lower credit scores are more likely to file claims. So, keep that credit score healthy, folks. It can save you money in more ways than you think.

Availability of Insurance During Hurricane Season

Moratoriums on New Policies

Here’s a fun little wrinkle: during hurricane season, many insurance companies put the brakes on issuing new policies. It’s called a moratorium, and it basically means you’re outta luck if you’re trying to get insured right before a storm hits. They don’t want to get stuck insuring a bunch of properties that are about to get clobbered. Smart for them, not so great for you if you’re caught in a bind.

Existing Policy Renewals

Even if you already have a policy, don’t assume you’re in the clear. Insurance companies can (and sometimes do) decide not to renew policies, especially in high-risk areas. So, keep an eye on your renewal date and be prepared to shop around if your current insurer gives you the boot. The key is to stay proactive.

The Florida Hurricane Catastrophe Fund (FHCF)

Okay, this is Florida’s secret weapon (sort of). The FHCF is basically a big pot of money that helps insurance companies pay out claims after a hurricane. It’s designed to keep the insurance market stable and prevent companies from going bankrupt after a major storm. It helps, but it’s not a magic bullet. We still need to do our part.

Finding Affordable Homeowner’s Insurance in Florida

Shopping Around and Comparing Quotes

This is the golden rule of insurance. Don’t just go with the first quote you get. Shop around. Get quotes from multiple companies. Compare coverage, deductibles, and premiums. You might be surprised at the difference in prices. It takes some time and effort, but it can save you a bundle.

Increasing Deductibles

As we talked about before, bumping up your deductible can lower your premium. Just make sure you can actually afford to pay that deductible if you ever need to file a claim. There’s no point in saving money on your premium if you’re gonna be totally broke when a hurricane rips off your roof.

Mitigation Measures

Want to impress your insurance company? Invest in wind mitigation measures. Hurricane shutters, reinforced roofs, impact-resistant windows – these things can make a big difference in how much you pay. Not only do they protect your home, but they also show your insurer that you’re serious about reducing risk.

Working with an Independent Insurance Agent

Independent agents are like insurance matchmakers. They work with multiple insurance companies, so they can shop around for the best rates on your behalf. They can also help you understand the fine print and make sure you’re getting the right coverage for your needs. Plus, they do all the heavy lifting for you. Sounds good, right?

Navigating the homeowner’s insurance landscape in Florida, especially during hurricane season, can feel overwhelming. But by understanding the factors that drive up costs, taking proactive steps to mitigate risk, and shopping around for the best rates, you can protect your property and your wallet. Don’t wait until a hurricane is bearing down on you to start thinking about insurance. Plan ahead, be prepared, and you’ll sleep a little easier knowing you’re covered. Now, go get those quotes!