“Home insurance premium

Artikel Terkait Home insurance premium

Pengantar

Dalam kesempatan yang istimewa ini, kami dengan gembira akan mengulas topik menarik yang terkait dengan Home insurance premium. Ayo kita merajut informasi yang menarik dan memberikan pandangan baru kepada pembaca.

Table of Content

Video tentang Home insurance premium

Home insurance, also known as homeowners insurance, is a crucial safety net that safeguards your property and belongings against unforeseen events like fire, theft, and natural disasters. However, the cost of this protection, determined by your home insurance premium, can vary significantly. Understanding the factors influencing your premium is key to securing affordable and adequate coverage.

:max_bytes(150000):strip_icc()/homeowners-insurance-guide_final-88e7d3469dcc4920977498f08564b234.png)

This comprehensive guide delves into the intricacies of home insurance premiums, explaining how they are calculated, the factors that affect them, and how you can potentially lower your costs while maintaining sufficient protection.

Understanding Home Insurance Premiums

Your home insurance premium is the amount you pay periodically (typically monthly or annually) to your insurance provider in exchange for coverage. This payment secures a contract where the insurer agrees to compensate you for covered losses or damages to your property. The premium isn’t a fixed amount; it’s dynamically calculated based on a multitude of factors, all aimed at assessing the risk the insurer takes in covering your property.

Factors Influencing Your Home Insurance Premium

Several key factors contribute to the calculation of your home insurance premium. These factors are carefully analyzed by insurance companies using sophisticated actuarial models to determine the likelihood and potential cost of claims.

-

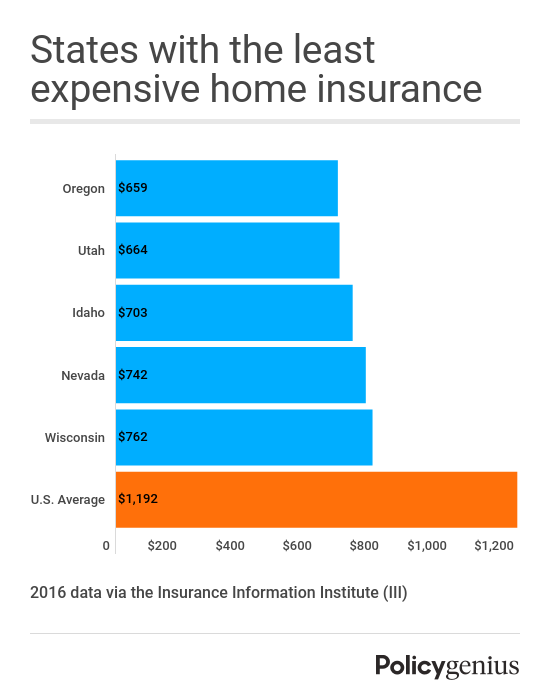

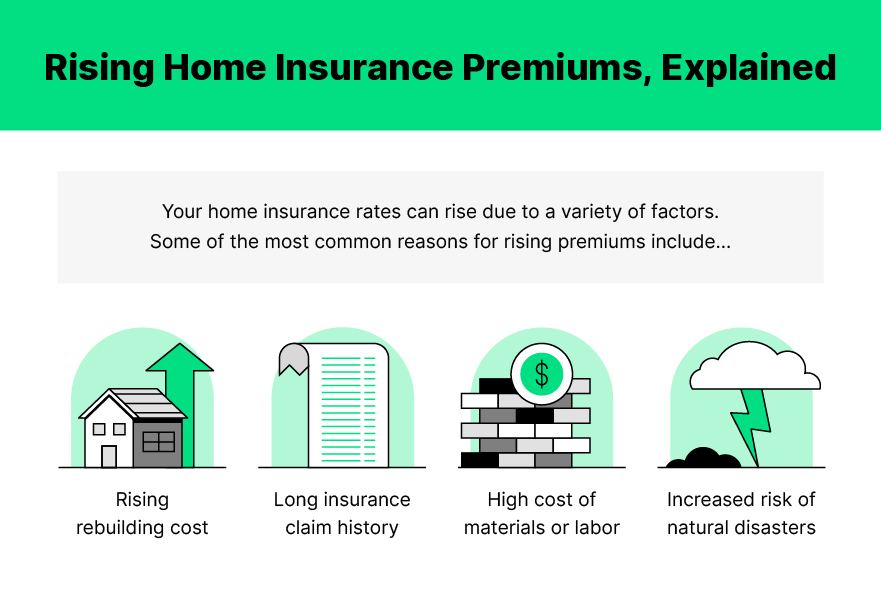

Location: Your home’s location is a significant factor. Homes in areas prone to natural disasters like hurricanes, earthquakes, wildfires, or floods will generally command higher premiums due to the increased risk of damage. The crime rate in your neighborhood also plays a role; higher crime rates lead to higher premiums due to the increased risk of theft or vandalism.

Home Value: The replacement cost of your home is a crucial determinant of your premium. A more expensive home requires a higher premium because the potential payout in case of damage is substantially larger. Insurance companies often use professional appraisals or automated valuation models to determine the accurate replacement cost.

-

Coverage Amount: The amount of coverage you choose directly impacts your premium. Higher coverage amounts mean higher premiums, as you’re paying for protection against greater potential losses. It’s essential to choose coverage that adequately protects your home’s value and your belongings, but avoid over-insuring, as this will unnecessarily increase your premium.

-

Deductible: Your deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in. Choosing a higher deductible lowers your premium, as you’re accepting more financial responsibility in case of a claim. However, a higher deductible means a larger upfront cost if you need to file a claim. Carefully weigh the trade-off between premium savings and potential out-of-pocket expenses.

-

Home Features: Certain features of your home can influence your premium. For example, homes with fire-resistant materials, updated electrical systems, and security systems may qualify for lower premiums due to reduced risk. Similarly, the age and condition of your roof, plumbing, and heating systems can affect your premium. Regular maintenance and upgrades can positively impact your insurance cost.

-

Claims History: Your past claims history is a significant factor. Frequent claims indicate a higher risk profile, leading to increased premiums. Insurance companies track your claims history, and multiple claims can result in higher premiums or even policy cancellation. Maintaining a clean claims history is crucial for keeping your premiums low.

-

Credit Score: In many states, your credit score is used as a factor in determining your insurance premium. A higher credit score often correlates with lower premiums, reflecting a lower perceived risk. This practice is controversial, but it remains prevalent in the insurance industry.

-

Insurance Company: Different insurance companies have different underwriting practices and risk assessments. Comparing quotes from multiple insurers is crucial to finding the best premium for your needs. Factors like company size, financial stability, and customer service should also be considered when choosing an insurer.

-

Type of Policy: The type of home insurance policy you choose influences your premium. Basic policies offer essential coverage, while comprehensive policies provide broader protection, including coverage for additional perils and higher liability limits. The extent of coverage directly impacts the premium.

-

Discounts: Many insurers offer discounts to incentivize responsible homeownership. These discounts can include discounts for bundling home and auto insurance, installing security systems, having smoke detectors, and being a long-term customer. Inquire about available discounts to potentially lower your premium.

Strategies for Lowering Your Home Insurance Premium

While you can’t control all the factors influencing your premium, you can take proactive steps to potentially lower your costs:

-

Improve Your Home’s Security: Installing security systems, smoke detectors, and other safety features can significantly reduce your risk profile and qualify you for discounts.

-

Maintain Your Home: Regular maintenance and timely repairs can prevent costly damages and reduce the likelihood of claims.

-

Shop Around: Compare quotes from multiple insurers to find the most competitive premium. Use online comparison tools to streamline the process.

-

Increase Your Deductible: A higher deductible reduces your premium, but remember to assess your ability to pay a larger out-of-pocket expense in case of a claim.

-

Bundle Your Policies: Many insurers offer discounts for bundling your home and auto insurance policies.

-

Explore Discounts: Inquire about available discounts, such as those for long-term customers, senior citizens, or military personnel.

-

Review Your Coverage Regularly: Your needs may change over time. Review your coverage annually to ensure you have adequate protection without overpaying.

Conclusion

Understanding the factors that influence your home insurance premium is crucial for securing affordable and adequate coverage. By taking proactive steps to mitigate risks, comparing quotes from multiple insurers, and exploring available discounts, you can effectively manage your home insurance costs while ensuring your valuable property remains protected. Remember, the goal is to find the right balance between cost and coverage, ensuring you have the protection you need without overspending. Regularly reviewing your policy and making necessary adjustments will contribute to long-term financial stability and peace of mind.

Penutup

Dengan demikian, kami berharap artikel ini telah memberikan wawasan yang berharga tentang Home insurance premium. Kami berharap Anda menemukan artikel ini informatif dan bermanfaat. Sampai jumpa di artikel kami selanjutnya!