“Home insurance policy

Artikel Terkait Home insurance policy

Pengantar

Dalam kesempatan yang istimewa ini, kami dengan gembira akan mengulas topik menarik yang terkait dengan Home insurance policy. Mari kita merajut informasi yang menarik dan memberikan pandangan baru kepada pembaca.

Table of Content

Video tentang Home insurance policy

Protecting this investment is paramount, and that’s where home insurance comes in. A home insurance policy, also known as homeowners insurance or hazard insurance, is a contract between you (the policyholder) and an insurance company. This contract promises financial protection against unforeseen events that could damage your property or cause you liability. Understanding the intricacies of your policy is crucial to ensure you’re adequately protected. This comprehensive guide will delve into the various aspects of home insurance, helping you navigate the complexities and make informed decisions.

I. Types of Home Insurance Policies:

The type of home insurance policy you need depends largely on your specific circumstances, including the type of property you own (single-family home, condo, townhouse), its location, and the level of coverage you require. Common types include:

-

HO-3 (Special Form): This is the most common type of homeowners insurance policy. It provides open-peril coverage for your dwelling and other structures (like a detached garage) meaning it covers damage from virtually any cause except those specifically excluded in the policy. Personal property is covered on a named-peril basis, meaning it only covers damage from specific events listed in the policy (e.g., fire, wind, theft).

-

HO-5 (Comprehensive Form): This policy offers the broadest coverage, providing open-peril coverage for both your dwelling and personal property. It’s the most comprehensive protection available, but also typically the most expensive.

HO-4 (Contents Broad Form): This policy is designed for renters and covers their personal belongings against specified perils. It doesn’t cover the building itself, as that’s the responsibility of the landlord’s insurance.

-

HO-6 (Condominium Unit Owners): This policy is specifically for condominium owners. It covers the interior of the condo unit and personal property, but not the building’s structure itself, which is covered by the condo association’s master policy.

-

HO-8 (Modified Coverage Form): This policy is designed for older homes that may be difficult to insure at full replacement cost due to their age and condition. It provides coverage for repair costs rather than full replacement value.

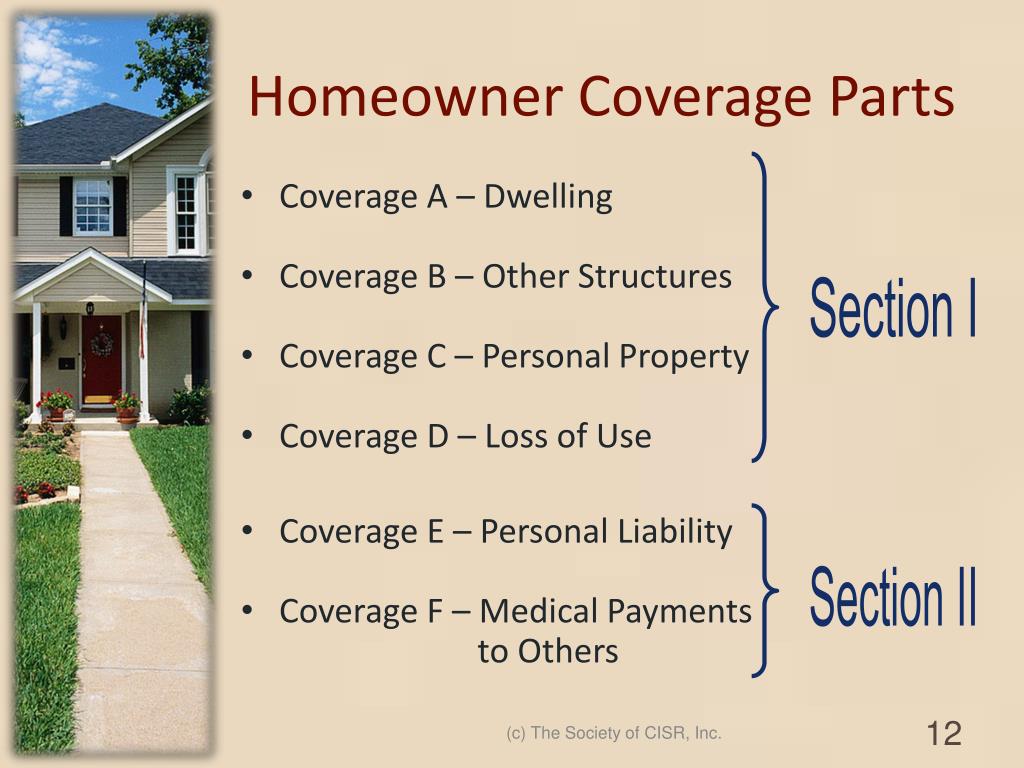

II. Key Components of a Home Insurance Policy:

A standard home insurance policy comprises several key components:

-

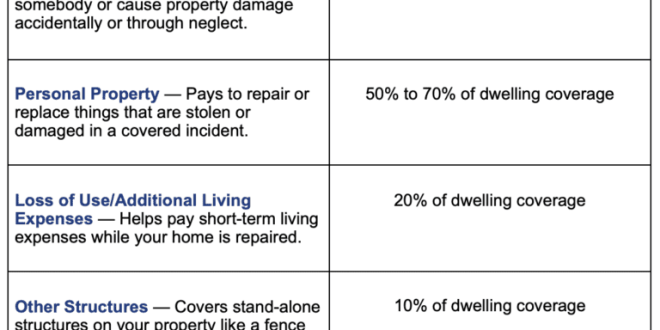

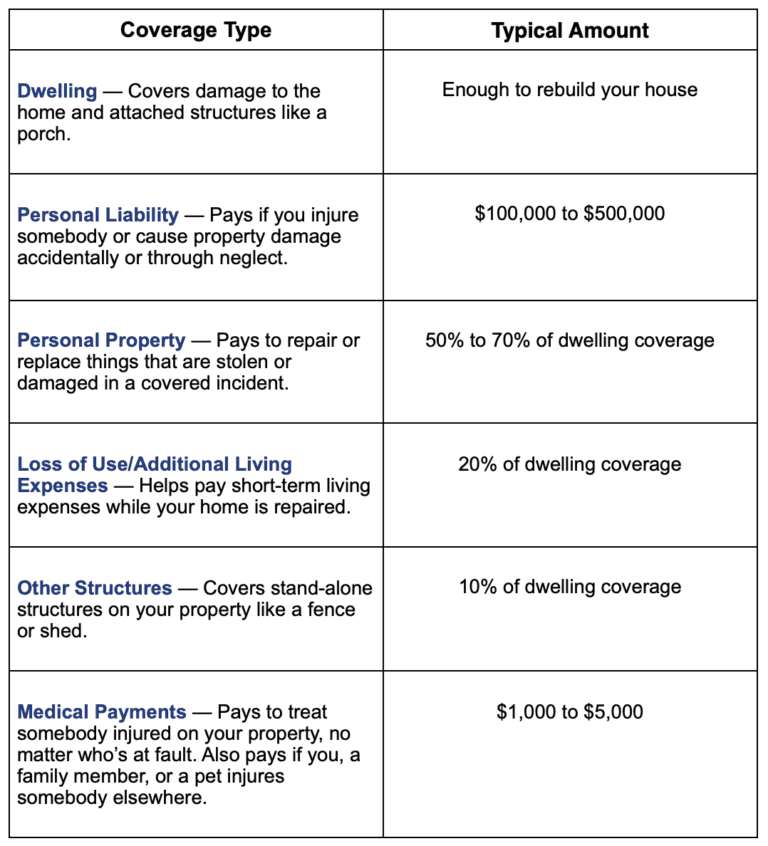

Coverage A: Dwelling: This covers the cost of repairing or rebuilding your home in case of damage from covered perils. The coverage amount is typically based on the replacement cost of your home, not its market value.

-

Coverage B: Other Structures: This covers detached structures on your property, such as a garage, shed, or fence. The coverage amount is usually a percentage (e.g., 10%) of the dwelling coverage.

-

Coverage C: Personal Property: This covers your belongings inside and outside your home, such as furniture, clothing, electronics, and jewelry. Coverage is typically based on actual cash value (ACV), which is the replacement cost minus depreciation, or replacement cost (RC), which covers the full cost of replacing your items.

-

Coverage D: Loss of Use: This covers additional living expenses if your home becomes uninhabitable due to a covered peril. This can include temporary housing, meals, and other necessary expenses.

-

Coverage E: Personal Liability: This protects you from financial liability if someone is injured on your property or if you cause damage to someone else’s property.

-

Coverage F: Medical Payments to Others: This covers medical expenses for guests or others who are injured on your property, regardless of your liability.

III. Factors Affecting Home Insurance Premiums:

Several factors influence the cost of your home insurance premiums:

-

Location: Homes in areas prone to natural disasters (hurricanes, earthquakes, wildfires) will generally have higher premiums.

-

Age and Condition of Your Home: Older homes may require more expensive repairs, leading to higher premiums. Proper maintenance can help lower your costs.

-

Coverage Amount: Higher coverage amounts will result in higher premiums.

-

Deductible: A higher deductible (the amount you pay out-of-pocket before insurance coverage kicks in) will result in lower premiums.

-

Credit Score: In many states, your credit score is a factor in determining your premiums. A higher credit score typically leads to lower premiums.

-

Claims History: A history of filing insurance claims can increase your premiums.

-

Security Features: Homes with security systems, fire alarms, and other safety features may qualify for discounts.

IV. Understanding Exclusions and Limitations:

No home insurance policy covers everything. Common exclusions include:

-

Flooding: Flood insurance is typically purchased separately.

-

Earthquakes: Earthquake insurance is also usually a separate policy.

-

Normal Wear and Tear: Damage caused by gradual deterioration is not covered.

-

Intentional Acts: Damage caused deliberately by the policyholder is not covered.

-

Specific Perils (depending on the policy type): As mentioned, some policies only cover specific perils, not all potential causes of damage.

V. Filing a Claim:

If you experience a covered loss, you should contact your insurance company immediately. Be prepared to provide detailed information about the incident, including photos and documentation of the damage. The claims process can vary depending on the insurer and the complexity of the claim.

VI. Choosing the Right Home Insurance Policy:

Choosing the right home insurance policy requires careful consideration of your individual needs and circumstances. Here are some tips:

-

Compare Quotes: Obtain quotes from multiple insurance companies to compare coverage and prices.

-

Review Policy Documents Carefully: Don’t just skim the policy; read it thoroughly to understand the coverage, exclusions, and limitations.

-

Consider Your Needs: Determine the level of coverage you need based on the value of your home and belongings.

-

Ask Questions: Don’t hesitate to ask your insurance agent any questions you may have.

-

Review Your Policy Regularly: Your needs may change over time, so it’s important to review your policy periodically and make adjustments as necessary.

VII. Additional Coverages:

Many homeowners choose to add additional coverages to their policies for enhanced protection:

-

Guaranteed Replacement Cost: This coverage guarantees that your home will be rebuilt even if the cost exceeds the policy’s coverage limit.

-

Personal Liability Umbrella Policy: This provides additional liability coverage beyond the limits of your home insurance policy.

-

Scheduled Personal Property: This provides specific coverage for high-value items such as jewelry or artwork.

-

Identity Theft Protection: This coverage helps with the costs associated with recovering from identity theft.

VIII. Maintaining Your Home Insurance Coverage:

To maintain adequate home insurance coverage, consider these actions:

-

Regularly update your policy: As your home’s value increases or your possessions change, update your policy to reflect these changes. This ensures you have sufficient coverage in case of a loss.

-

Maintain accurate records: Keep detailed records of your belongings, including receipts, photos, and appraisals. This will be invaluable in the event of a claim.

-

Conduct regular home maintenance: Preventative maintenance can significantly reduce the risk of damage and potential claims.

-

Review your policy annually: Make sure your coverage still meets your needs and that you haven’t inadvertently let your coverage lapse.

Conclusion:

Home insurance is a vital component of responsible homeownership. Understanding the nuances of your policy, from the types of coverage to the factors influencing premiums, empowers you to make informed decisions and protect your most valuable asset. By carefully reviewing your policy, comparing quotes, and addressing your specific needs, you can secure the peace of mind that comes with knowing you’re adequately protected against unforeseen events. Remember that this is a complex subject, and consulting with a qualified insurance professional is always recommended to ensure you have the right coverage for your unique situation.

Penutup

Dengan demikian, kami berharap artikel ini telah memberikan wawasan yang berharga tentang Home insurance policy. Kami mengucapkan terima kasih atas waktu yang Anda luangkan untuk membaca artikel ini. Sampai jumpa di artikel kami selanjutnya!